Credit Card Terminology Explained: APR, Credit Limit, Balance & More

Credit cards are an everyday financial tool for many Australians—but the terminology can sometimes be a little confusing. Whether you're managing your first card or simply looking to improve your financial literacy, understanding the key terms on your statement can empower you to use credit responsibly and effectively. In this guide, we break down the most common credit card terms—like APR, credit limit, balance and more—so you can make informed decisions, compare offers confidently, and know exactly what you're signing up for when you apply for a credit card online.

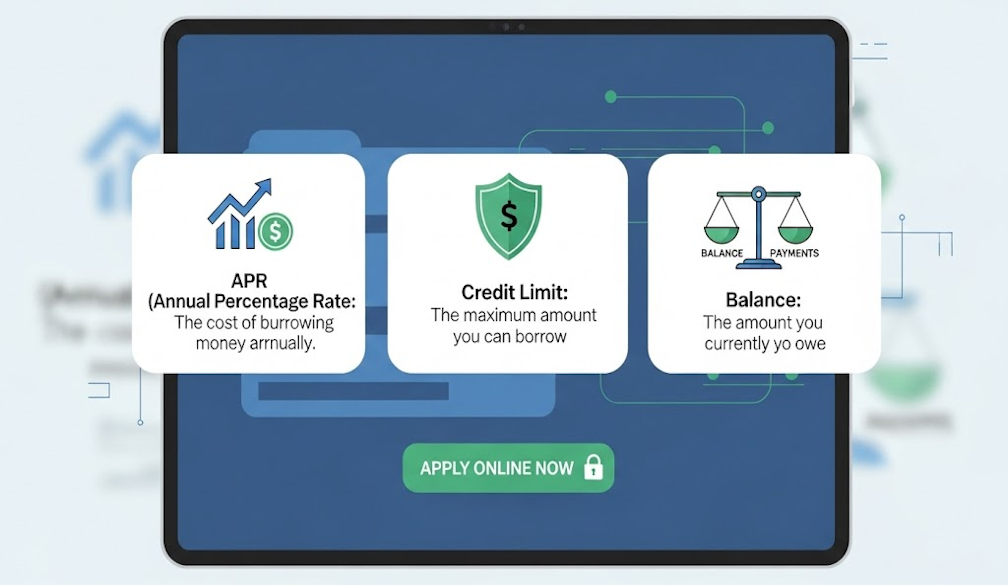

Annual Percentage Rate (APR)

APR is the annual cost of borrowing on your credit card, expressed as a percentage. It includes interest charges and may also include certain fees, giving you a more comprehensive view of the true cost of using your card if you don’t pay the balance in full each month.

- Introductory APR: Some cards offer a lower or 0% APR for an initial period.

- Purchase APR: The interest rate applied to everyday purchases.

- Cash Advance APR: A higher interest rate that applies when you withdraw cash using your credit card.

Tip: Always check whether an advertised rate is promotional or ongoing, and how long any introductory period lasts.

Credit Limit

Your credit limit is the maximum amount you can borrow on your card. This limit is set by the lender based on factors like your income, credit history, and overall financial health.

- Available Credit: The amount you have left to spend, calculated by subtracting your current balance from your credit limit.

- Over-Limit Fees: Some cards charge fees if you exceed your credit limit, while others may simply decline the transaction.

Keeping your balance well below the limit can positively impact your credit score and help avoid unmanageable debt.

Outstanding Balance

Your outstanding balance is the total amount you currently owe on your credit card. This may include purchases, cash advances, interest charges, and any applicable fees.

- Statement Balance: What you owed at the end of your billing cycle.

- Current Balance: What you owe at any given moment, including recent activity.

- Minimum Payment: The smallest amount you need to pay to keep your account in good standing—but paying only the minimum can lead to more interest charges over time.

Interest-Free Period

Many credit cards offer an interest-free period on purchases—typically between 44 to 55 days. To benefit, you’ll need to pay off your statement balance in full by the due date each month. If you carry a balance, this interest-free window often disappears, and new purchases may start accruing interest immediately.

Cash Advance

A cash advance is when you use your credit card to withdraw cash or transfer funds. It usually incurs:

- No interest-free period

- A higher interest rate (Cash Advance APR)

- Additional fees (e.g. a percentage of the amount withdrawn)

Cash advances can be convenient but are generally best avoided unless absolutely necessary.

Rewards Program

Some credit cards offer rewards programs where you earn points, cashback, or other benefits for spending on the card. While these perks can add value, it’s important not to overspend just to chase rewards, especially if it leads to interest charges.

Balance Transfer

A balance transfer involves moving your existing credit card debt to another card—often one with a lower or 0% introductory interest rate. This can be a smart way to consolidate debt and reduce interest costs, but it’s crucial to check for:

- Transfer fees

- The duration of the introductory rate

- The interest rate after the promotional period ends

Credit cards can be powerful financial tools when used wisely, but understanding the fine print is key to staying in control

Knowing terms like APR, credit limit, and balance empowers you to manage your spending, avoid unnecessary fees, and make the most of your credit options. If you're considering your next step, it’s easier than ever to apply for a credit card online with providers offering flexible, transparent options tailored to your financial goals.