China's demand for seaborne coal is set to drop fast and far. Australia should take note.

- Written by: Jorrit Gosens, Research Fellow, Australian National University

China’s plans to boost energy security and cut carbon emissions mean this year’s sudden boom for Australian coal exporters is just a blip.

Our new research[1] explores the double pressures of China’s plans[2] to bolster energy security in the wake of the Russian invasion of Ukraine while aiming to hit net zero within 40 years.

Our model suggests that if China sticks to its current climate pledges, thermal coal imports will drop by a quarter within three years from 210 megatonnes (Mt) in 2019 to 155Mt by 2025. That means Australian exports could fall by 20% by 2025, while Australian coking coal exports could fall even more. This is in stark contrast to predictions of stable demand or even continued growth by the Australian government.

How could this happen so quickly, when coal prices have roughly tripled compared to the last decade? In short, better infrastructure. China has invested in major rail projects, including a direct rail line to a major coking coal mine in Mongolia, as well as increasing use in scrap steel.

Coal’s wild ride in the volatile 2020s

The last few years have been a rollercoaster for coal producers. For Australia’s major coal exporters, it’s been a wild ride.

After falling for some years, coal prices fell sharply as the COVID pandemic and resulting lockdowns led to a sharp decline in energy consumption. Adding to the pressure, China banned the imports of coal from Australia.

Read more: Suddenly we are in the middle of a global energy crisis. What happened?[3]

Before the disruption of the 2020s, China bought roughly a quarter of Australia’s exports of thermal coal (burned in power stations) and a similar share of coking coal exports (used in steelmaking).

In 2021, coal consumption and emissions shot back up after an unexpectedly strong economic rebound. Coal supplies were also disrupted due to COVID-related restrictions and workforce shortages. Together, these factors tripled coal spot prices to US$300 a tonne for thermal coal and US$450 a tonne for coking coal.

In China, the sudden scarcity of coal led to Australian coal held at its ports rushed through customs clearance. While the import ban formally remains in place, government data[4] shows Australia has managed to divert most of its coal exports to countries such as India, Japan, South Korea, and Taiwan.

Chinese energy security means a drop in Australian seaborne coal

We expect all of these issues to be fairly short-lived. The big picture is China’s goal of net-zero emissions by 2060, and its interim target to peak emissions before 2030.

How will it do that? By expanding renewable power generation, increasing coal power station efficiency while reducing dependence on coal power longer term, and increased use of steel scrap. Better steel recycling will reduce demand for new steel, which requires two of Australia’s key exports, iron ore and coking coal. Reduced demand will inevitably affect China’s need to import coal.

For the next few years, coal will remain vital to China’s industrial strength and ability to power its cities. That’s where energy security comes in. China has invested heavily in freight railway capacity, in order to bring its own coal to its power and steel plants more cheaply.

It has also built rail connections to Tavan Tolgoi in neighbouring Mongolia, one of the world’s largest and cheapest sources of high-quality coking coal. With the new railway capacity, coking coal can now travel 1,200 kilometres to China’s steelmaking heartland in Hebei province, near Beijing.

Mongolia’s enormous Tavan Tolgoi mine now has a direct rail link to Hebei province.

Brücke-Osteuropa, Public domain, via Wikimedia Commons, CC BY[5][6]

Mongolia’s enormous Tavan Tolgoi mine now has a direct rail link to Hebei province.

Brücke-Osteuropa, Public domain, via Wikimedia Commons, CC BY[5][6]

We took these factors into account in modelling different scenarios for Australian coal. We assume China will follow through on its existing climate policies.

In our scenarios, the largest losses would be borne by the biggest current suppliers of thermal coal to China. Number one exporter Indonesia could see its exports almost halved by 2025, falling from 125Mt in 2019 to as low as 65Mt.

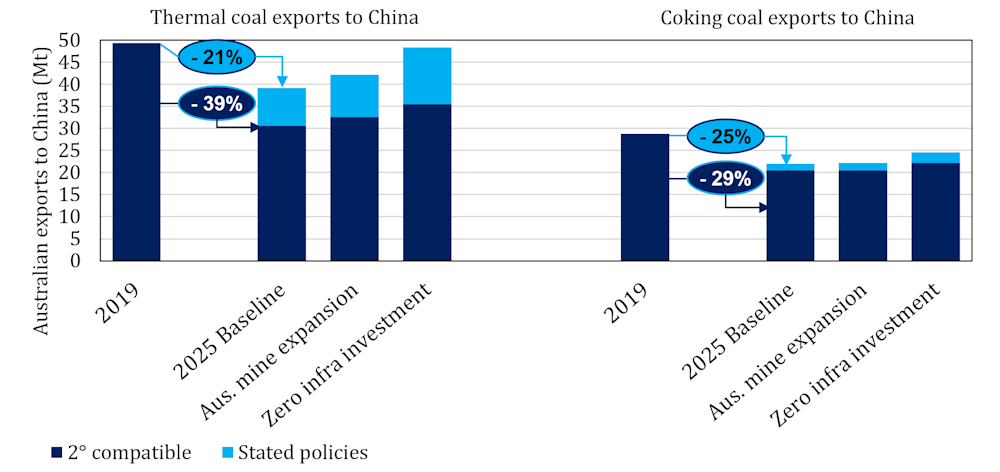

Overall, China’s thermal coal imports should fall rapidly, dropping from 210Mt in 2019 to 155Mt by 2025. That means even if the embargo on Australian coal is lifted, our exports of thermal coal to China could still fall from 50Mt in 2019 to between 40 and 30 Mt in that timeframe, depending on China’s level of climate ambition. Coking coal exports could fall from 30Mt to as low as 20Mt.

Three of the scenarios we modelled for Australian coal exports to China, assuming the embargo lifts. Zero infrastructure investment refers to a counter-factual in which China had not built additional freight railways and ports.

Supplied, Author provided

Three of the scenarios we modelled for Australian coal exports to China, assuming the embargo lifts. Zero infrastructure investment refers to a counter-factual in which China had not built additional freight railways and ports.

Supplied, Author provided

If the embargo remains in place, the drop in Chinese demand for seaborne coal will mean China’s current suppliers will shift back to competing in the global market, and push out Australian suppliers. The net effect on Australian exports will likely be comparable.

We also explored the scenario in which all of Australia’s currently planned coal mine expansions actually go ahead. We found even in this scenario, there would be little impact on the loss of market share in China. By contrast, if Mongolian mines expand, our model predicts they would readily fill Chinese market demand at the expense of Australian coking coal imports.

To get these predictions, we ran a cost optimisation model with greatly improved representations of transport networks. The model finds the lowest cost at which different mines could supply all of China’s power and steel plants. We did not factor in political choices based on energy security or concerns about “just transitions”, such as, for instance, a Chinese push to limit the pain for its substantial coal mining and trucking workforce.

Read more: China's energy crisis shows just how hard it will be to reach net zero[7]

Overall, our model makes clear China’s demand for coal – expected to plateau or fall over the next few years – coupled with its expansion of domestic mine and transport capacity will reduce the role for Australian coal. The world’s top buyer of coal will increasingly be able to supply its power and steel plants with domestically mined coal at competitive costs.

In turn, that means it will be less costly for China to depend on what it considers to be volatile markets. It will also be easier to impose politically motivated import restrictions on suppliers from what it considers unfriendly countries.

China’s ability to cut seaborne coal imports will grow further if its government increases its decarbonisation ambitions. These plans will be a key influence on the the remaining demand for seaborne coal.

Australia’s government and investors would be wise to consider these macro-level changes and plans as they look ahead, rather than focusing on short term gains from current market volatility.

Alex Turnbull, fund manager at Keshik Capital, contributed to this article and was a co-author of the published research. He personally holds no coal stocks.

References

- ^ new research (www.cell.com)

- ^ China’s plans (www.reuters.com)

- ^ Suddenly we are in the middle of a global energy crisis. What happened? (theconversation.com)

- ^ government data (publications.industry.gov.au)

- ^ Brücke-Osteuropa, Public domain, via Wikimedia Commons (commons.wikimedia.org)

- ^ CC BY (creativecommons.org)

- ^ China's energy crisis shows just how hard it will be to reach net zero (theconversation.com)