Finder’s RBA survey: 86% of experts forecast rate hike

As soaring cost of living continues to squeeze household budgets, both homeowners and renters are in for little relief, according to a new Finder poll.

In this month’s Finder RBA Cash Rate Survey™, 28 experts and economists weighed in on future cash rate moves and other issues relating to the state of the economy.

Most panellists (86%, 24/28) believe the cash rate will change on Tuesday, while 28% (8/28) believe there will be at least two cash rate increases before the end of the year.

Graham Cooke, head of consumer research at Finder, said Australians were already feeling the pinch.

“The economy is at a precipice and some families are really starting to struggle financially with the cost of living – and for those with a home loan, it could get a lot worse.

“Lifting the cash rate is good news for savers, and will help to slow Australia’s runaway property market, but those with a home loan are in line for several further cost increases,” Cooke said.

David Robertson of Bendigo Bank said the RBA is likely to increase rates in 25 basis point-increments steadily over the next 9 months, until we approach a cash rate of around 2%.

“They will be careful not to overshoot with policy tightening and risk a hard landing, but inflation will rise further due to supply issues so they have more work to do," Robertson said.

What a 2.50% cash rate will cost mortgage holders

Interestingly, 2 in 5 experts (39%, 7/18) say the cash rate will peak at 2.50% or above.

The vast majority (71%, 15/21) predict the peak will happen sometime in 2023.

Cooke said there is a possibility that the June rate increase will be higher than expected – 40 basis points rather than 25.

“However, only one third of our economists thought this was likely. Gradual increases are more probable,” Cooke said.

A cash rate at 2.50% would cost the average homeowner an eye-watering $8,592 each year.

The increase would raise the average Aussie homeowners' repayments $716 a month – from $2,324 to $3,040.

“Many homeowners are going to struggle to meet these new payment requirements. If you are at risk, it might be worth locking in a low fixed rate now, before rates rise further,” Cooke said.

| Cash rate | Example variable home loan interest rate | Monthly payment on $600,000 home loan* | Monthly difference | Difference over 1 year |

|---|---|---|---|---|

| 0.35% (current rate) |

2.35% | $2,324 | N/A | N/A |

| 0.75% (predicted rate as of June 7) |

2.75% | $2,449 | $125 | $1,500 |

| 2.50% (predicted peak) |

4.50% | $3,040 | $716 | $8,592 |

| Source: Finder *Based on the ABS average home loan balance, on a principal and interest loan over 30 years. |

||||

Rental affordability could be in crisis

Some tenants have been pushed to the brink by recent price hikes in the rental market. CoreLogic data shows median weekly rents increased by 9% over the past 12 months.

Worryingly, over half of experts (53%, 8/15) forecast similar or even higher growth in rents over the next 12 months. This includes 27% (4/15) who think rental growth will exceed 9%, and 27% (4/15) who think rental growth will be around 9%.

According to Finder’s Consumer Sentiment Tracker – a nationally representative survey of more than 30,000 respondents – over a third of Australian renters (35%) struggled to pay their rent in May.

Cooke said a myriad of factors, including record low rental vacancy rates, were driving up costs.

“Rental costs were driven down last year due to lockdowns, but are quickly bouncing back. On top of that, construction costs are continuing to soar, and rental vacancies reached record low levels in May.

“The corresponding spike in rental costs is leaving tenants with very little money leftover for necessities,” Cooke said.

Michael Yardney from Metropole Property Strategists said renters were doing it tough.

“We are in a rental crisis with vacancy rates at record lows, a shortage of rental properties as many investors have sold up over the last year or two, and there is very little new investment stock coming onto the market,” Yardney said.

Some economists, like Jakob M Madsen from the University of Western Australia, expect the rental crisis to subside over the coming year.

“House prices and therefore rents will decrease in the next months due to the increasing cash rate,” Madsen said.

Tim Reardon from Housing Industry Association agreed, noting, “The influx of new housing completions will moderate the rate of increase this year. There is also a return to higher density living underway.”

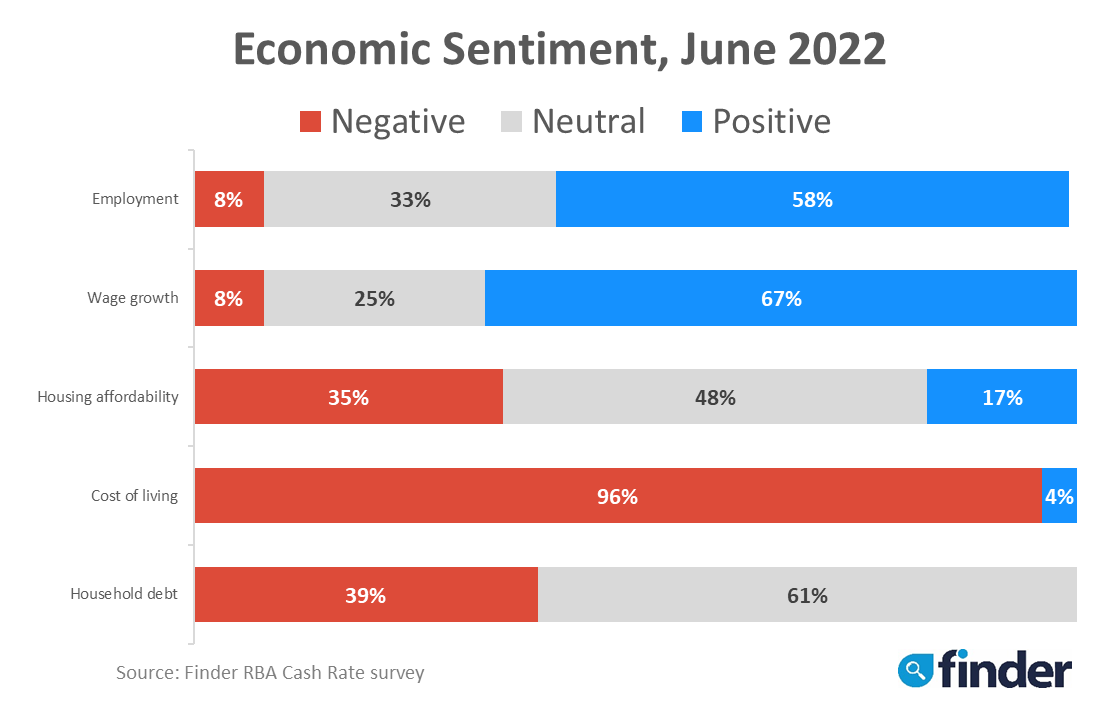

Finder's Economic Sentiment Tracker gauges experts' confidence in 5 key indicators: housing affordability, employment, wage growth, cost of living and household debt.

Negativity towards cost of living grew from 80% last month to 96% in June.

Experts not in favour of Labor’s ‘Help to Buy’ scheme

The newly elected government’s Help to Buy scheme, designed to help more Australians buy homes by sharing the upfront purchase costs, will contribute up to 40% of the purchase price of 10,000 properties each year.

However two-thirds of experts (65%, 11/17) don’t believe the policy is a good idea, with most claiming that strategies to increase housing supply would be more effective.

Rich Harvey from Propertybuyer said it was a demand side policy that only serves to bolster demand.

“Policies should be focussed on the supply side, and getting wages higher for new trades and university degrees so that younger people can climb the salary ladder faster to afford their first home,” Harvey said.

Dale Gillham from Wealth Within believes it could have negative consequences for mortgage affordability.

“They are just helping more people who can't afford a property to get into debt, and this will only increase housing prices,” Gillham said.

Leanne Pilkington from Laing+Simmons had a different view, noting that first home buyers need all the help they can get.

“While limited in scope, this scheme may help some people to enter the market,” Pilkington said.

Graham Cooke notes that there are few popular options.

“Previous surveys show that both Labor and the LNP’s housing affordability solutions were unpopular with economists. While Labor’s scheme proved decisive, the LNP’s policy of allowing buyers to hack into their retirement savings could have been very damaging.”

*Experts are not required to answer every question in the survey

Here’s what our experts had to say:

Dr Andrew Wilson, My Housing Market: "The RBA will likely raise rates again for June although the level of increase has become problematic given the nature of the data released in recent weeks is likely to challenge the Bank’s assumptions. Predictably disappointing wages data, low jobs growth, another fall in the participation rate, another sharp decline in the savings rate, falling disposable income levels and a moderate GDP performance will be food for thought for the RBA who are hoping to avoid a hard landing in its attempt to curb inflation. Recessionary clouds are already gathering in other advanced economies that increased rates higher and earlier than Australia."

Craig Emerson, Emerson Economics: "The RBA has begun the tightening process and there's nothing in the inflation outlook to suggest it has finished."

Dr Angela Jackson, Impact Economics and Policy: "[It’s] clear further tightening [is required] given capacity constraints in the labour market and general price rises now evident across the economy."

Cameron Kusher, REA Group: "It's clear the RBA like many other central banks around the world are behind the inflation curve and after increasing interest rates for the first time since 2010 last month, I fully expect a follow-up increase in June."

Peter Munckton, Bank of Queensland: "Inflation is too high."

Rich Harvey, Propertybuyer: "RBA is now committed to raising the cash rate to counter very strong inflation pressure, but will not be raising rates in rapid succession – they will take a cautious approach." Rich Harvey

David Zammit, Mortgage Choice: "I believe it’s a question of by how much, rather than if, the Reserve Bank will raise the cash rate at its June monetary policy meeting. Most lenders on the Mortgage Choice panel passed on last month’s cash rate rise on their variable rate loan products and we have also seen some increases to fixed rate loan pricing."

Tim Reardon, Housing Industry Association: "August will allow the RBA to see one more quarter of CPI data (in July), given the official data thus far still points to inflation being largely concentrated in fuel prices and home building costs, and wage growth relatively weak. Global financial and economic uncertainties are also high for the rest of the year."

Shane Oliver, AMP: "Inflation is running well above target and likely to get worse. Unemployment at 3.9% is effectively at full employment. Wage growth is picking up. There is a danger that the longer inflation stays high and demand is strong, inflation expectations will rise, making it even harder to get inflation back down. So the RBA needs to continue the process of normalising interest rates."

Leanne Pilkington, Laing+Simmons: "There’s an expectation that a further interest rate increase is coming. For the housing market, we’re in unusual territory where it’s a case of the sooner the better, so a return to market normality can ensue and so borrowers can know where they stand."

Nicholas Gruen, Lateral Economics: "I'm not sure."

Sarah Hunter, KPMG: "The data continues to confirm that inflationary pressures are building, and that the supply disruptions globally are at least semi-permanent. Furthermore, the RBA Board signalled in May that they expect to progress with rate rises from here. Together, this suggests another 0.25% increase in the cash rate."

Brodie Haupt, WLTH: "With continued uncertainty and rising pressure from inflation, I think it is likely there will be continual changes to the cash rate throughout the year."

Peter Boehm, Pathfinder Consulting: "The RBA has no choice but to implement cash rate increases for the remainder of the calendar year. It is going to be quite painful for those households with mortgages and variable rate debt."

Dale Gillham, Wealth Within: "With rates haven just risen and signs the property market is coming off, I think the RBA might play a wait and see game for a few months."

Mathew Tiller, LJ Hooker: "Strong inflationary pressures are not expected to subside anytime soon and with unemployment now under 4.0% I expect the RBA will lift rates multiple times over the remainder of 2022."

Jonathan Chancellor, The Daily Telegraph: "The RBA will make another rise as it seeks to normalise rates."

Tim Nelson, Griffith University: "The RBA has indicated it will seek to gradually return rates to levels more akin to longer term experience."

David Robertson, Bendigo Bank: "The RBA is very likely to increase rates in 0.25% increments steadily over the next 9 months until we approach a cash rate of around 2%. They will be careful not to overshoot with policy tightening and risk a hard landing, but inflation will rise further due to supply issues so they have more work to do."

Harry Murphy Cruise, Moody's Analytics: "The RBA’s task is as much about managing expectations as it is taking heat out of the buoyant economy. Short-term inflation expectations are rising and the RBA needs to tame those gains. The May rate hike confirms that the RBA is acting on rising inflationary pressures even if much of the price rises are outside the RBA’s sphere of influence (notably food and energy). We expect a 40 basis point hike in June, bringing the cash rate to 0.75% to reinforce this commitment. The speed of further interest rate normalisation will rely on how well businesses and families react to these higher borrowing costs, as well as the pace of real wage gains."

Mark Brimble, Griffith University: "The RBA is keen to normalise rates in the short term."

Saul Eslake, Corinna Economic Advisory Pty Ltd: "The RBA needs to get monetary policy settings back to 'neutral' fairly quickly given the outlook for inflation."

Geoffrey Harold Kingston, Macquarie University: "To try and get in front of the curve."

Nicholas Frappell, ABC Refinery: "Policy normalisation has only just begun. The RBA senses wage pressures are also emerging in a tight labour market."

Noel Whittaker, QUT: "Inflation is rife, and I think they now think they were too soft on the last rise."

Stephen Halmarick, Commonwealth Bank: "Need to tighten policy due to the inflation environment."

Michael Yardney, Metropole Property Strategists: "The RBA realises that Australia's inflation has caught them by surprise so they're now keen to get it under control."

Jakob B. Madsen, University of Western Australia: "The low unemployment and high inflation that is likely to remain above the RBA target for a while."