How housing made rich Australians 50% richer, leaving renters and the young behind – and how to fix it

- Written by: Brendan Coates, Program Director, Economic Policy, Grattan Institute

Compared to the rest of the world, income inequality is not particularly high[1] in Australia, nor is it getting much worse – until you include housing.

Rising housing costs have dramatically widened the gap between what Australians on high and low incomes can afford. Rising home prices paired with plummeting rates of homeownership are driving up wealth inequalities.

If we want to address inequality, we will have to fix housing.

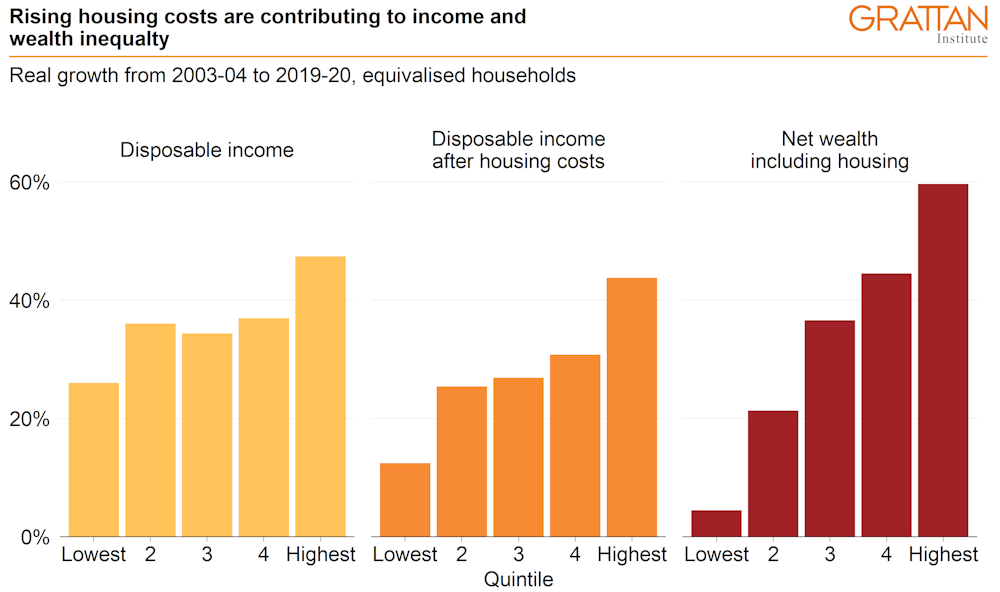

Housing is draining the incomes of the poor

People on low incomes, who are increasingly renters, are spending more of their incomes on housing.

The inflation-adjusted incomes for the lowest fifth of households increased by about 26% between 2003-04 and 2019-20. But more than half of this was chewed up by skyrocketing housing costs, with post-housing incomes climbing only 12%.

In contrast, the real incomes for the highest fifth of households increased by 47%, and their after-housing incomes by almost as much: 43%.

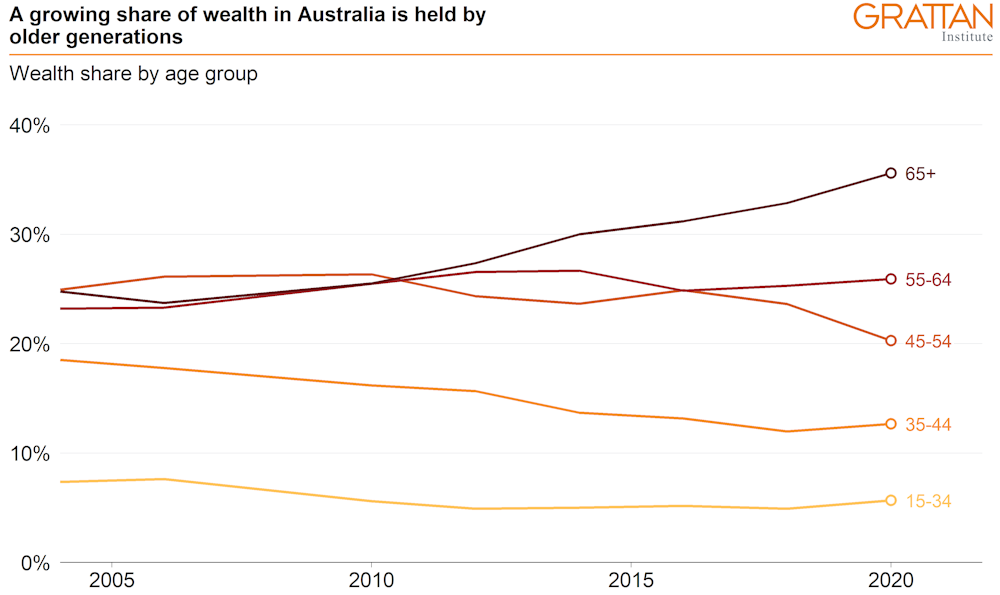

Housing is driving wealth inequality

Wealth inequality in Australia is still below the OECD average but has been climbing for two decades.

While average full-time earnings have doubled over the past half-century, home prices have quadrupled.

It’s made more and more Australians millionaires. In 2019-20, fully one-quarter of homeowning households reported net wealth exceeding A$1 million[3].

Read more: Renters spend 10 times as much on housing as petrol. Where's their relief?[4]

Rising asset prices over the following two years, albeit now starting to reverse, mean this figure is almost certainly higher now.

Median net wealth for non-homeowning households is a lowly $60,000.

Since 2003-04, the wealth of high-income households has grown by more than 50%, much of that due to increasing property values. By contrast, the wealth of low-income households – mostly non-homeowners – has grown by less than 10%.

Housing is driving up capital income

Rents used to make up just 2% of national income in Australia. Now they’re almost 10%. This explains more than a quarter of the rise in the capital share of income in Australia since 1960.

As housing has become more expensive, it’s the wealthier Australians who own more housing who have benefited the most.

Economists Josh Ryan-Collins and Cameron Murray estimate[5] that up until June 2019, in more than half of the previous 30 quarters the median Sydney home earnt more than the median full-time worker.

In other words, a relatively low-risk, low-effort investment provided greater returns than a year of hard work.

Housing is creating a Jane Austen world

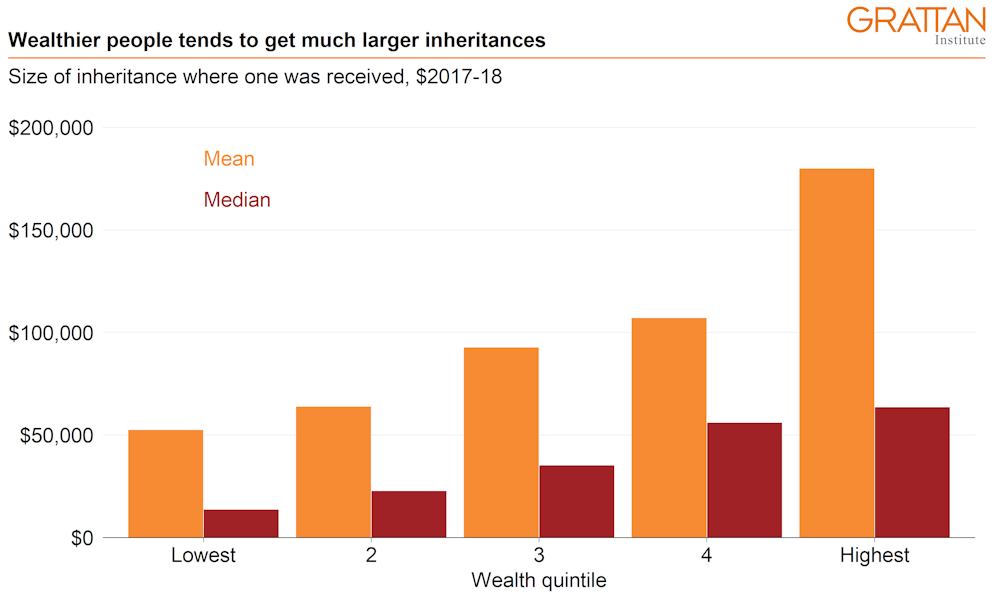

The growing divide between the housing “haves” and “have nots” is being entrenched as wealth is passed onto the next generation.

And the swelling of national household wealth to a total of $14.9 trillion – increasingly in the hands of the baby boomers and older generations – means there is an awfully big pot of wealth to be passed on.

Source: ABS Survey of Income and Housing microdata

Big inheritances boost the jackpot from the birth lottery, the jackpot that underlies the Jane Austen novels set in the early 19th century. It was a world in which none of the rich got rich by working[6].

Among the Australians who received an inheritance over the past decade, the wealthiest fifth received on average three times as much as the poorest fifth.

Source: ABS Survey of Income and Housing microdata

Big inheritances boost the jackpot from the birth lottery, the jackpot that underlies the Jane Austen novels set in the early 19th century. It was a world in which none of the rich got rich by working[6].

Among the Australians who received an inheritance over the past decade, the wealthiest fifth received on average three times as much as the poorest fifth.

Notes: Data on inheritances by wealth of recipient is not available from the probate records, so we use data from HILDA on self-reported inheritances. Wealth captured only in 2002, 2006, 2010, and 2014 surveys. Wealth quintile based on most recently-captured wealth information for an individual.

Source: HILDA Survey, 2002 to 2017

And inheritances are increasingly coming later in life. As the miracles of modern medicine have extended life expectancy, the most common age in which to receive an inheritance has been late fifties or early sixties – much later than when the money is needed to ease the mid-life squeeze of housing and children.

Large intergenerational wealth transfers can change the shape of society. They mean that a person’s economic position relates more to who their parents are than to their own talent or hard work.

To unwind inequality, we need to make housing less expensive.

Fix tax, but build more houses

The federal government should start by reducing the capital gains tax discount and abolishing negative gearing.

The effect on property prices would be modest – roughly 2% lower than otherwise[7] – but the impact on home ownership would be a lot larger over time, as first home buyers begin to outbid investors at auctions.

However, housing inequality won’t really fall until more housing is built.

Australia hasn’t built enough housing for its growing population, because the construction of new homes has been all too often constrained by planning rules[8].

Read more:

A brief history of the mortgage, from its roots in ancient Rome to the English 'dead pledge' and its rebirth in America[9]

Planning is a state responsibility, and easing planning restrictions is hard for state governments because many residents don’t want more homes near theirs.

That’s why the federal government should make it worth the states’ while via the new Housing Accord that sets targets for new construction and pays the states for each home built above a baseline.

Grattan Institute calculations suggest that if an extra 50,000 homes were built each year for the next ten years, national home prices and rents would be 10-20%[10] lower than otherwise.

Auckland’s[11] large-scale re-zoning in 2016 saw an extra 5% of the housing stock built in five years. We could do something like it here.

Correction: an earlier version of this piece put the value of national household wealth at $14.9 billion. The value is $14.9 trillion.

References^ not particularly high (www.pc.gov.au)^ Source: ABS Survey of Income and Housing microdata (www.abs.gov.au)^ exceeding A$1 million (grattan.edu.au)^ Renters spend 10 times as much on housing as petrol. Where's their relief? (theconversation.com)^ estimate (www.tandfonline.com)^ got rich by working (inequality.org)^ roughly 2% lower than otherwise (grattan.edu.au)^ planning rules (grattan.edu.au)^ A brief history of the mortgage, from its roots in ancient Rome to the English 'dead pledge' and its rebirth in America (theconversation.com)^ 10-20% (grattan.edu.au)^ Auckland’s (cdn.auckland.ac.nz)Authors: Brendan Coates, Program Director, Economic Policy, Grattan Institute

Notes: Data on inheritances by wealth of recipient is not available from the probate records, so we use data from HILDA on self-reported inheritances. Wealth captured only in 2002, 2006, 2010, and 2014 surveys. Wealth quintile based on most recently-captured wealth information for an individual.

Source: HILDA Survey, 2002 to 2017

And inheritances are increasingly coming later in life. As the miracles of modern medicine have extended life expectancy, the most common age in which to receive an inheritance has been late fifties or early sixties – much later than when the money is needed to ease the mid-life squeeze of housing and children.

Large intergenerational wealth transfers can change the shape of society. They mean that a person’s economic position relates more to who their parents are than to their own talent or hard work.

To unwind inequality, we need to make housing less expensive.

Fix tax, but build more houses

The federal government should start by reducing the capital gains tax discount and abolishing negative gearing.

The effect on property prices would be modest – roughly 2% lower than otherwise[7] – but the impact on home ownership would be a lot larger over time, as first home buyers begin to outbid investors at auctions.

However, housing inequality won’t really fall until more housing is built.

Australia hasn’t built enough housing for its growing population, because the construction of new homes has been all too often constrained by planning rules[8].

Read more:

A brief history of the mortgage, from its roots in ancient Rome to the English 'dead pledge' and its rebirth in America[9]

Planning is a state responsibility, and easing planning restrictions is hard for state governments because many residents don’t want more homes near theirs.

That’s why the federal government should make it worth the states’ while via the new Housing Accord that sets targets for new construction and pays the states for each home built above a baseline.

Grattan Institute calculations suggest that if an extra 50,000 homes were built each year for the next ten years, national home prices and rents would be 10-20%[10] lower than otherwise.

Auckland’s[11] large-scale re-zoning in 2016 saw an extra 5% of the housing stock built in five years. We could do something like it here.

Correction: an earlier version of this piece put the value of national household wealth at $14.9 billion. The value is $14.9 trillion.

References^ not particularly high (www.pc.gov.au)^ Source: ABS Survey of Income and Housing microdata (www.abs.gov.au)^ exceeding A$1 million (grattan.edu.au)^ Renters spend 10 times as much on housing as petrol. Where's their relief? (theconversation.com)^ estimate (www.tandfonline.com)^ got rich by working (inequality.org)^ roughly 2% lower than otherwise (grattan.edu.au)^ planning rules (grattan.edu.au)^ A brief history of the mortgage, from its roots in ancient Rome to the English 'dead pledge' and its rebirth in America (theconversation.com)^ 10-20% (grattan.edu.au)^ Auckland’s (cdn.auckland.ac.nz)Authors: Brendan Coates, Program Director, Economic Policy, Grattan Institute