Thanks to APRA, it's about to become harder to get a mortgage. Here's why

- Written by: Warren Hogan, Industry Professor, University of Technology Sydney

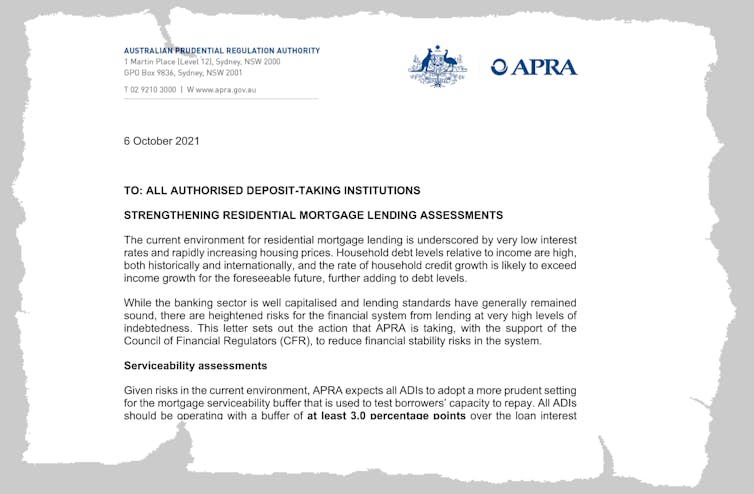

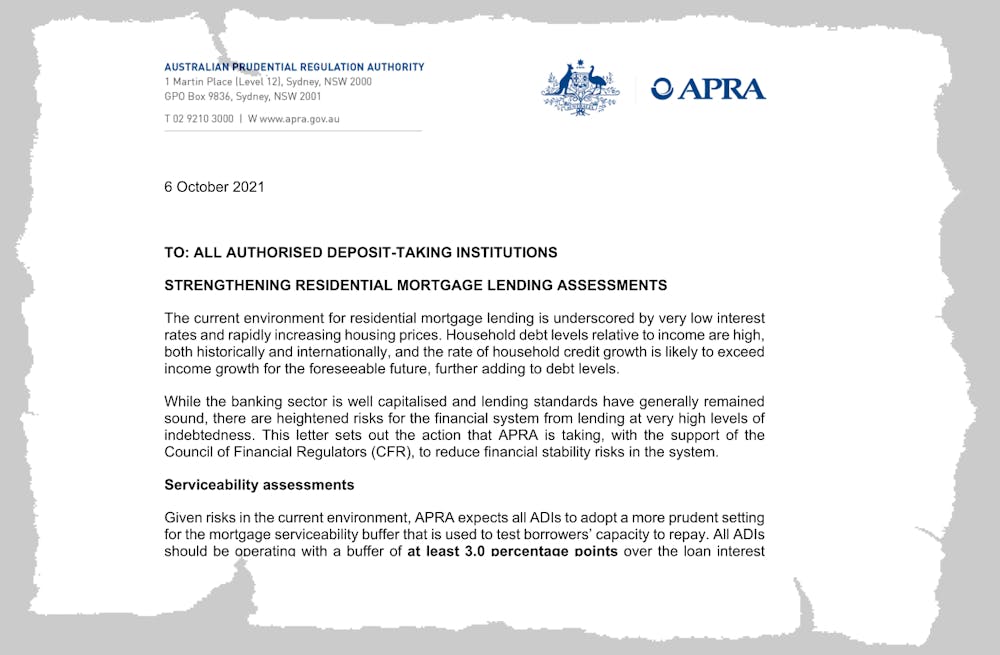

On Wednesday the Australian Prudential Regulation Authority wrote to each of Australia’s home lenders asking them to make it just a little bit harder for Australians to get mortgage.

The letter, addressed to so-called authorised deposit-taking institutions, asked them to adopt a serviceability buffer “at least 3.0 percentage points over the loan interest rate”.

Reserve Bank Governor Philip Lowe has indicated rates shouldn’t need to rise until 2024.

APRA is taking out insurance.

With global inflation pressures building, there is a risk not only that rates climb go earlier than the Reserve Bank is signalling, but that the increases will be substantial, given how far rates are below normal.

The small adjustment to serviceability buffers has been described as a tap on the brakes of the housing market[5].

While this might be part of the impact, APRA’s objective is to reduce the vulnerability of individual borrowers and banks themselves to an increase in interest rates down the track.

The biggest impact on the most leveraged borrowers.

The most leveraged borrowers tend to be first home buyers and investors. APRA believes investors will be affected the most because first home buyers tend to be “more constrained by the size of their deposit”.

Investors are more leveraged and often have multiple loans to which the new requirement will be applied.

Insurance, for 2022

So far, investors have been less prominent than usual in the market upturn.

APRA seems to think this is about to change. Investors stayed away when home prices began climbing late last year, but returned to the market this year and have been increasingly active.

Read more:

Home prices are climbing alright, but not for the reason you might think[6]

Unchecked, low interest rates combined with Australia’s favourable taxation treatment of property investment could drive a new wave of investor-driven demand well into 2022.

Low interest rates are making low-yielding real estate extremely attractive.

APRA may be preparing itself for twin threats it sees around the corner – a new wave of investor-driven home price inflation, and the first increase in official interest rates in more than a decade.

References^ Australian Prudential Regulation Authority (www.apra.gov.au)^ fairly modest (www.apra.gov.au)^ Reserve Bank not for turning. No rate hike until unemployment near 4.5% (theconversation.com)^ 2024 (theconversation.com)^ tap on the brakes of the housing market (www.afr.com)^ Home prices are climbing alright, but not for the reason you might think (theconversation.com)Authors: Warren Hogan, Industry Professor, University of Technology Sydney

Reserve Bank Governor Philip Lowe has indicated rates shouldn’t need to rise until 2024.

APRA is taking out insurance.

With global inflation pressures building, there is a risk not only that rates climb go earlier than the Reserve Bank is signalling, but that the increases will be substantial, given how far rates are below normal.

The small adjustment to serviceability buffers has been described as a tap on the brakes of the housing market[5].

While this might be part of the impact, APRA’s objective is to reduce the vulnerability of individual borrowers and banks themselves to an increase in interest rates down the track.

The biggest impact on the most leveraged borrowers.

The most leveraged borrowers tend to be first home buyers and investors. APRA believes investors will be affected the most because first home buyers tend to be “more constrained by the size of their deposit”.

Investors are more leveraged and often have multiple loans to which the new requirement will be applied.

Insurance, for 2022

So far, investors have been less prominent than usual in the market upturn.

APRA seems to think this is about to change. Investors stayed away when home prices began climbing late last year, but returned to the market this year and have been increasingly active.

Read more:

Home prices are climbing alright, but not for the reason you might think[6]

Unchecked, low interest rates combined with Australia’s favourable taxation treatment of property investment could drive a new wave of investor-driven demand well into 2022.

Low interest rates are making low-yielding real estate extremely attractive.

APRA may be preparing itself for twin threats it sees around the corner – a new wave of investor-driven home price inflation, and the first increase in official interest rates in more than a decade.

References^ Australian Prudential Regulation Authority (www.apra.gov.au)^ fairly modest (www.apra.gov.au)^ Reserve Bank not for turning. No rate hike until unemployment near 4.5% (theconversation.com)^ 2024 (theconversation.com)^ tap on the brakes of the housing market (www.afr.com)^ Home prices are climbing alright, but not for the reason you might think (theconversation.com)Authors: Warren Hogan, Industry Professor, University of Technology Sydney