Cash rate rise to cost the average homeowner $801 per month

Homeowners on a variable mortgage rate have been stung with yet another rate hike and can expect to pay thousands more in interest per year, according to Finder.

In this month’s Finder RBA Cash Rate Survey™, 36 experts and economists weighed in on future cash rate moves and other issues relating to the state of the economy.

Almost all experts (97%, 35/36) predicted a cash rate rise in September, with nearly two-thirds (64%, 23/36) correctly predicting the increase of 50 basis points from 1.85% to 2.35%.

It’s a heavy blow to mortgage holders on a variable interest rate – with monthly repayments up by almost one-third (29%) in only 5 months.

The majority of experts (69%, 25/36) expect the RBA to hold the cash rate next month in October.

Graham Cooke, head of consumer research at Finder, said the combined cash rate hikes will cost the average Aussie homeowner an additional $801 per month compared to what they were paying in April.

“This fifth rate rise since May piles on the pressure for Aussie homeowners, who will have almost $10,000 less to spend on groceries, clothing and holidays compared to only 6 months ago.”

|

Cash rate |

Average home loan rate* |

Average monthly repayment |

Average monthly increase since April |

Average annual repayment |

Average annual increase since April |

|

|

April 2022 |

0.10% |

3.45% |

$2,727 |

|

$32,728 |

|

|

August 2022 |

1.85% |

5.15% |

$3,337 |

$610 |

$40,045 |

$7,317 |

|

September 2022 (current rate as of 6 September) |

2.35% |

5.65% |

$3,528 |

$801 |

$42,336 |

$9,608 |

|

Source: Finder, RBA. *Owner-occupier variable discounted rate. Repayments based on the average loan of $611,158 in April 2022 (ABS data analysed by Finder). |

|

|||||

Cooke said borrowers who took out fixed rate home loans before the rate rises started won’t notice a difference straight away.

“Fixed loan holders are in for a big shock once that rate expires and their payments spike.

“Our figures show the average fixed-rate homeowner will be paying $600 extra per month come December.

“If you’re on a fixed rate, check now to see how much your repayments are likely to jump.”

Aussies squirrel away more as cost of living crisis continues

The Australian Prudential Regulation Authority (APRA) figures show that household bank deposits continued to increase in June by $2.9 billion compared to May.

Finder research found the average Australian had $39,439 in savings in August, compared to $22,565 in March.

Graham Cooke said some Aussies were drastically increasing how much cash they have stashed.

“While we have yet to see the desired economic impact of the rate cuts so far, one group will welcome the increase – Australian savers.

“Now is a great time to have excess cash in the bank. High interest savings accounts are offering rates of more than 3.30% per year.

“However we know not everyone has this luxury – Finder research shows almost 1 in 4 (24%) Aussie homeowners struggled to pay their mortgage in August,” Cooke said.

Rich Harvey from Propertybuyer said the majority of borrowers are ahead on repayments and have buffers in place.

“However these will dwindle rapidly if rates are ratcheted up too high," Harvey said.

Jeffrey Sheen from Macquarie University said in general, households will manage.

“But there may be too many marginal households that will struggle," Sheen said.

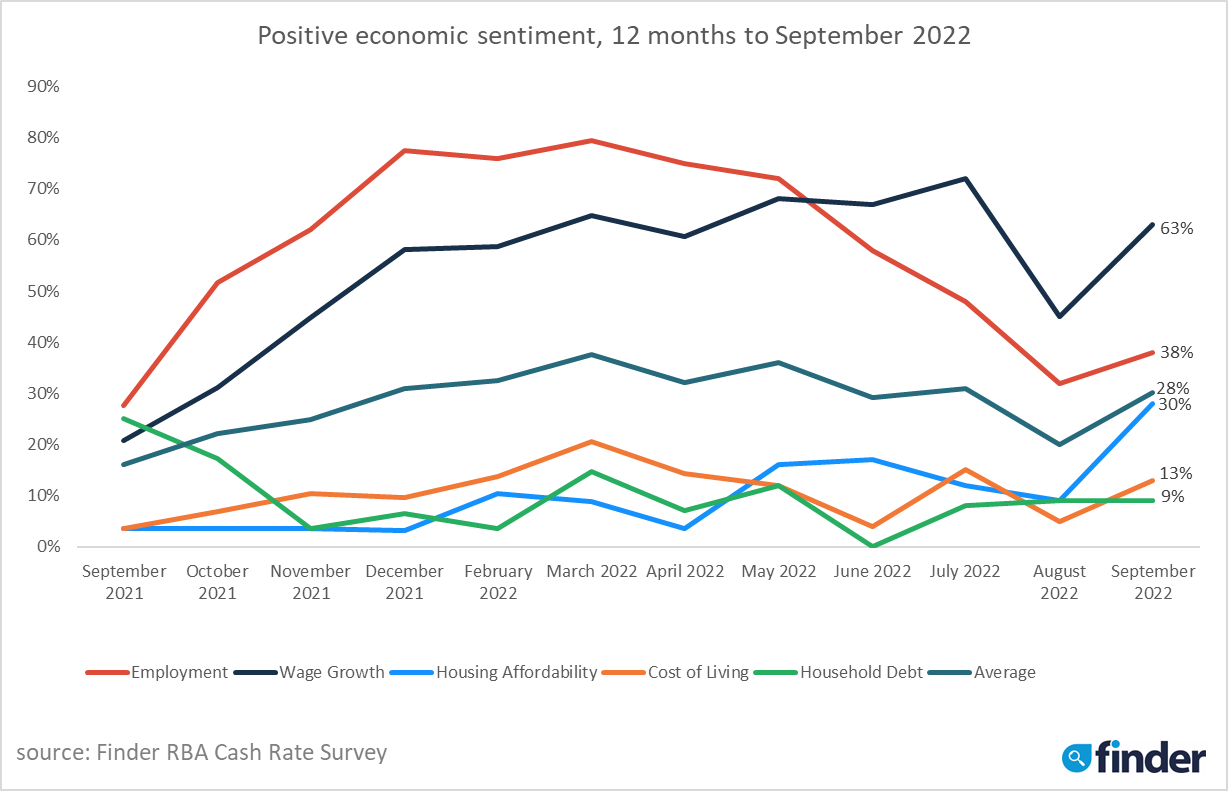

Experts split on the cash rate impact on wage growth

With wage growth continuing to lag behind inflation, just over half of panellists (53%, 16/30) say that rising interest rates are stopping businesses from giving workers pay rises.

That’s despite an increase in positivity towards wage growth in September.

Finder's Economic Sentiment Tracker gauges experts' confidence in 5 key indicators: housing affordability, employment, wage growth, cost of living and household debt.

Positivity towards almost all 5 indicators has increased since August, with wage growth seeing the biggest jump (45% to 63%).

Inflation likely to peak between 7% and 8%

Almost 3 in 4 experts who weighed in* (72%, 21/29) agree that the monthly consumer price index (CPI) will continue to increase and peak between 7% and 8%.

The majority of panellists (70%, 21/30) believe inflation will hit its peak by the end of 2022.

Angela Jackson from Impact Economics and Policy said international pressures would ease.

“However the flow through of higher prices and domestic demand pressures will push inflation higher by year end,” Jackson said.

Saul Eslake of Corinna Economic Advisory Pty Ltd said many of the global factors which have been a significant contributor to the rise in inflation over the past year appear to have peaked already.

“This should exert a downward influence on Australia's inflation rate next year.

“Additionally by next year, growth in domestic demand is likely to have slowed significantly making it more difficult for businesses to pass on cost increases in the form of higher prices," Eslake said.

*Experts are not required to answer every question in the survey

Here’s what our experts had to say:

Tim Reardon, Housing Industry Association (Hold): "November will allow the RBA to see one more CPI data print before their next upward move. It will also give them some more time to see the impact of their cash rate hikes to date."

Anthony Waldron, Mortgage Choice (Increase): "ABS data shows the labour market is continuing to tighten, and inflation remains high, so I expect to see another cash rate rise in September."

Mala Raghavan, University of Tasmania (Increase): "Inflation is still rising in Australia, fuelled by demand-driven and supply-side disruption shocks, which have a high possibility of pushing inflation beyond 7% by the end of this year."

Dr Andrew Wilson, My Housing Market (Increase): "Inflation rate too high on RBA benchmark and economy still booming."

Azeem Sheriff, CMC Markets Australia (Increase): "AU is still behind the curve and [there are] no signs of inflation slowing down or peaking. Energy prices will still remain high, so will need credit demand to reduce along with discretionary spending for inflation to cool."

Matthew Peter, QIC (Increase): "The RBA is now committed to lowering inflation, as are most other central banks. The Jackson Hole pronouncements have given the RBA little choice other than to raise rates by another 50 basis points at their September meeting to be followed by another 50 basis point hike in October."

Mathew Tiller, LJ Hooker Group (Increase): "The impact of recent cash rate increases have begun to impact property markets across the country; however, inflation across the rest of the economy remains a concern for the RBA. As such, the RBA will continue to increase the cash rate over the short term."

Sveta Angelopoulos, RMIT (Increase): "Inflationary impacts are continuing and remain an ongoing concern."

Angela Jackson, Impact Economics and Policy (Increase): "Expect the RBA to continue tightening until at least November, and not look to decrease until later in 2023."

Sarah Hunter, KPMG (Increase): "Although the drop in employment in July (albeit from a very strong increase in June) suggests that growth momentum is now easing, activity levels are still very high in absolute terms. The economy is testing the limits of its supply side capacity, and in this environment, inflationary pressures remain elevated. The RBA will be conscious of the need for further increases in the cash rate to tame these pressures, and an increase of at least 25 bps is a near certainty; the Board could choose to increase by 40 bps (to return the cash rate to its pre-COVID increments), but a 50bps increase looks marginally more likely."

Nicholas Gruen, Lateral Economics (Increase): "The bank is cranking up rates. I think they should take a breather to see more of the effects of past rate rises."

Leanne Pilkington, Laing+Simmons (Increase): "While not working to a pre-set path, the Reserve Bank has indicated it will increase rates further. The rate increases in recent months are yet to be fully felt by the market so we believe there’s a case for the Reserve Bank to take stock of the impacts to date."

Peter Munckton, Bank of Queensland (Increase): "Interest rates are too low, inflation is too high and the economy is doing well."

Brodie Haupt, WLTH (Increase): "The Reserve Bank will continue to increase the cash rate until the inflation begins to abate."

Malcolm Wood, Ord Minnett (Increase): "Robust growth continues allowing the RBA to return the cash rate to their estimate of the neutral level."

Mark Crosby, Monash University (Increase): "Still some way to get back to neutral rates, and expect 1 more 50 basis point, or 2x 25 basis point rises before year end."

Nicholas Frappell, ABC Refinery (Increase): "Wage growth appears to be accelerating as inflationary expectations act in combination with a tight labour market. Energy prices continue to influence factor prices elsewhere."

Tim Nelson, Griffith University (Increase): "RBA will continue to tighten monetary policy with a view to containing inflationary pressures. Given many of these pressures are beyond Australian control (i.e. oil prices, supply chain constraints abroad), limiting investment through monetary policy is less likely to be effective."

Shane Oliver, AMP (Increase): "The RBA is likely to raise rates by another 0.5% at its September meeting. Demand remains strong, capacity utilisation is at or around record levels and price pressures remain intense with inflation still high and likely to rise to around 7.5% by year end. As such the RBA remains under pressure to bring demand back into line with supply and to continue signalling that it is committed to its 2–3% inflation target in order to keep inflation expectations down."

Jason Azzopardi, Resimac (Increase): "Aligns with RBA narrative to rein in inflation. Clear this journey is not finished."

Sean Langcake, BIS Oxford Economics (Increase): "The RBA have indicated rates need to go higher before they enter 'neutral' territory. But the headwinds to activity are mounting, and we expect the Bank will pause to assess the impact of higher rates sooner rather than later."

David Robertson, Bendigo Bank (Increase): "Another 50 basis point RBA rate hike in September will take us closer to a neutral cash rate, before likely 0.25% increases in October and November. The RBA will remain on a tightening bias until core inflation is back near target, to try to minimise the risks of the global inflation shock."

Rich Harvey, Propertybuyer (Increase): "The RBA is on a dedicated mission to curtail inflation and is partially through the rate rising cycle to slow demand … but many of the pressures are on the supply side."

Jakob B Madsen, University of Western Australia (Increase): "Inflation is still above target and there is a risk that the inflation rate remains high unless RBA conducts an aggressive monetary policy."

Craig Emerson, Emerson Economics (Increase): "The RBA appears likely to go too hard too soon, necessitating a reverse direction in the first half of 2023."

Peter Boehm, Pathfinder Consulting (Increase): "It is highly likely the cash rate will be sitting around the 2.5% mark by year end. This means the RBA have to keep increasing rates over the next couple of months. No current economic or financial data has come to light which would cause the RBA to deviate off its stated path of rate increases to combat inflation – even though such a strategy will probably do more harm than good with limited positive impact on bringing prices down."

Geoffrey Harold Kingston, Macquarie University (Increase): "Bad inflation prints are likely in October this year and January next year. We may get a good print by October next year."

Dale Gillham, Wealth Within (Increase): "Whilst the RBA in past said it would not raise rates until next year, they have since made it reasonably clear this thinking has changed and that they will most likely continue to raise rates until the end of this year."

Stephen Halmarick, Commonwealth Bank (Increase): "Further tightening required to meet inflation objectives. Peak is expected to be 2.6% as per question below."

Jeffrey Sheen, Macquarie University (Increase): "There are signs that supply constraints are easing and that inflation will soon begin to moderate. Fortunately, inflation expectations seem to remain anchored. Meanwhile the RBA will continue for a few more months to normalise the cash rate, after which they will hold. To ensure a soft landing, a reduction in the rate may be seen to be required mid-2023."

Saul Eslake, Corinna Economic Advisory Pty Ltd (Increase): "The RBA still has some way to go in moving the cash rate to a level appropriate for an economy at full employment and with inflation well above its target range."

Michael Yardney, Metropole Property Strategists (Increase): "Interest rates are still at low, stimulatory levels and need to be raised to at least neutral or preferably higher levels to bring inflation under control."

Mark Brimble, Griffith University (Increase): "They will want to input a bit more pressure on rates re. inflation and demand and then settle to allow the 18-month transmission into the economy to occur. If global pressures don’t resolve (Ukraine, China and energy) then they may go again in Nov/Dec. If these things do resolve/start to resolve they are likely to pause, then a return to long-run fundamentals in the second half of next year will see stability or a slight easing."

Noel Whittaker, QUT (Increase): "The Reserve Bank has made it clear that they will keep increasing rates but won't go more than 50 basis points at a time."

Alan Oster, NAB (Increase): "RBA moving rates closer to normal, but aware not to overdo it."

Stephen Miller, GSFM (Increase): "Inflation will prove a little more intractable than markets currently contemplate."