At the heart of the budget is the sad truth the economy is weak. That’s one reason inflation will fall

- Written by: Aruna Sathanapally, Chief Executive, Grattan Institute, Grattan Institute

A central focus of this week’s budget is the treasury’s forecast for inflation.

By this time next year, inflation is projected to be back within the Reserve Bank’s 2-3% target range[1].

Inflation has dropped dramatically[2] from its peak of 7.8% just 18 months ago, but the last mile – getting from the present 3.6% to less than 3% – was always going to be the hardest.

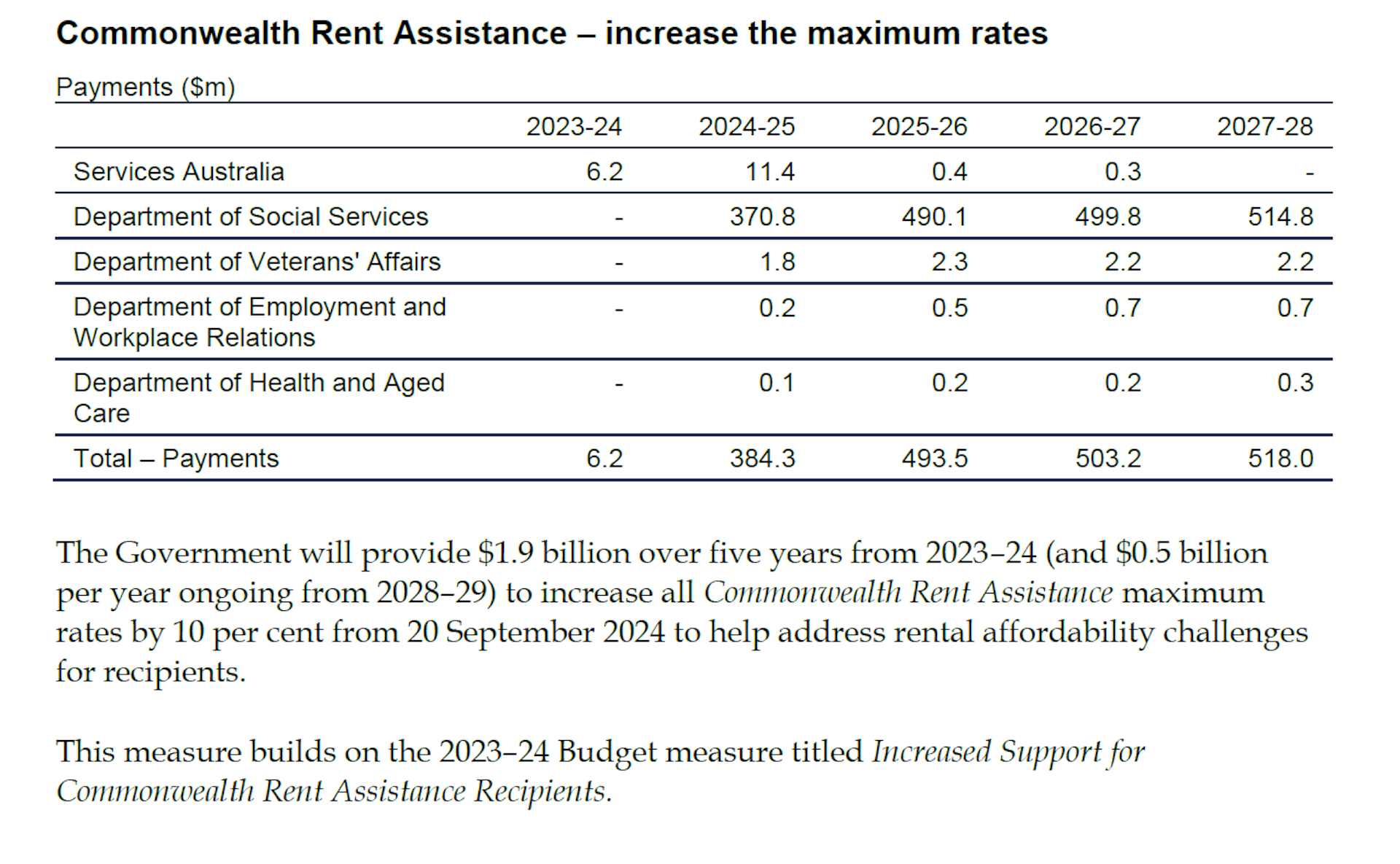

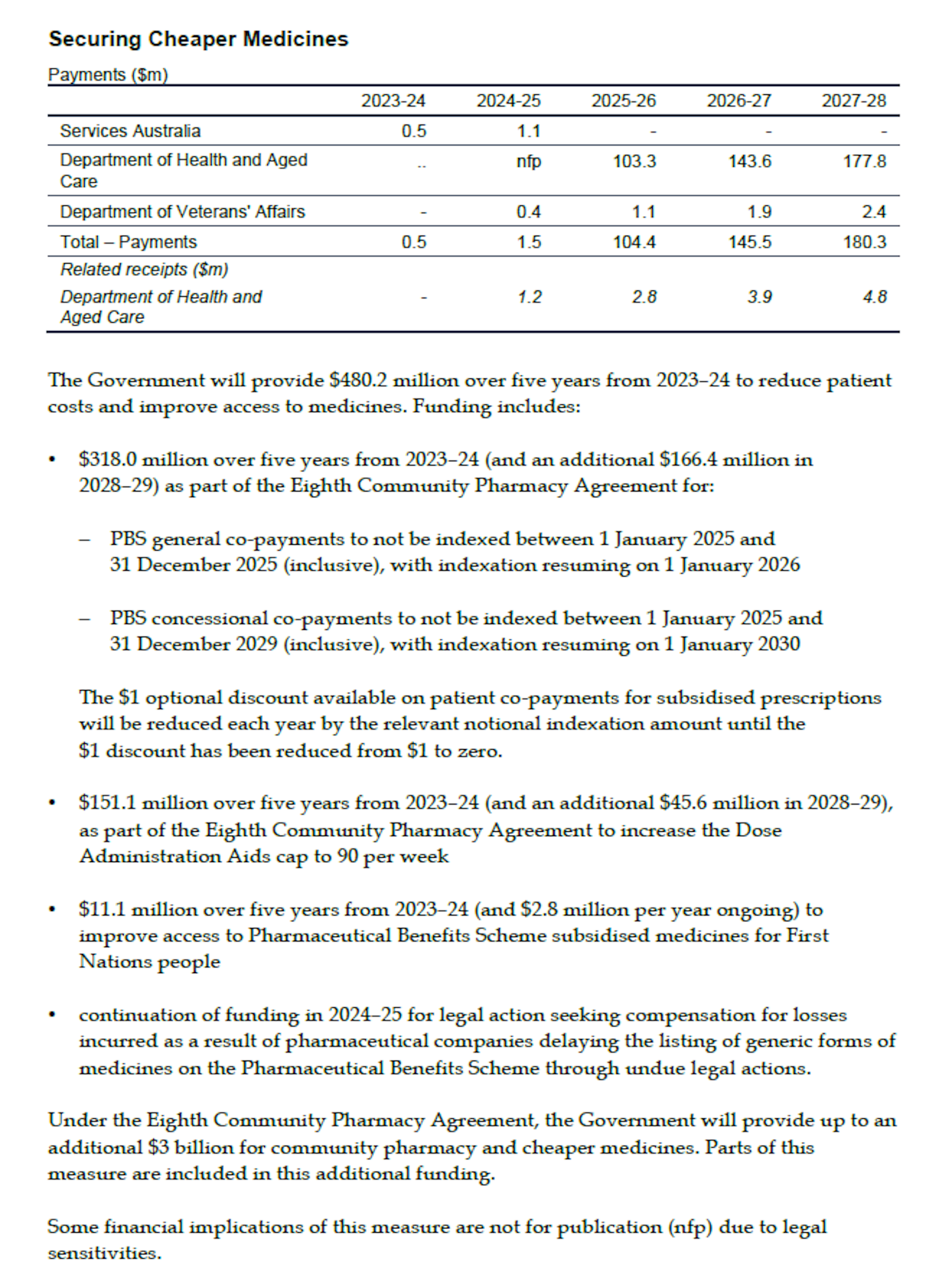

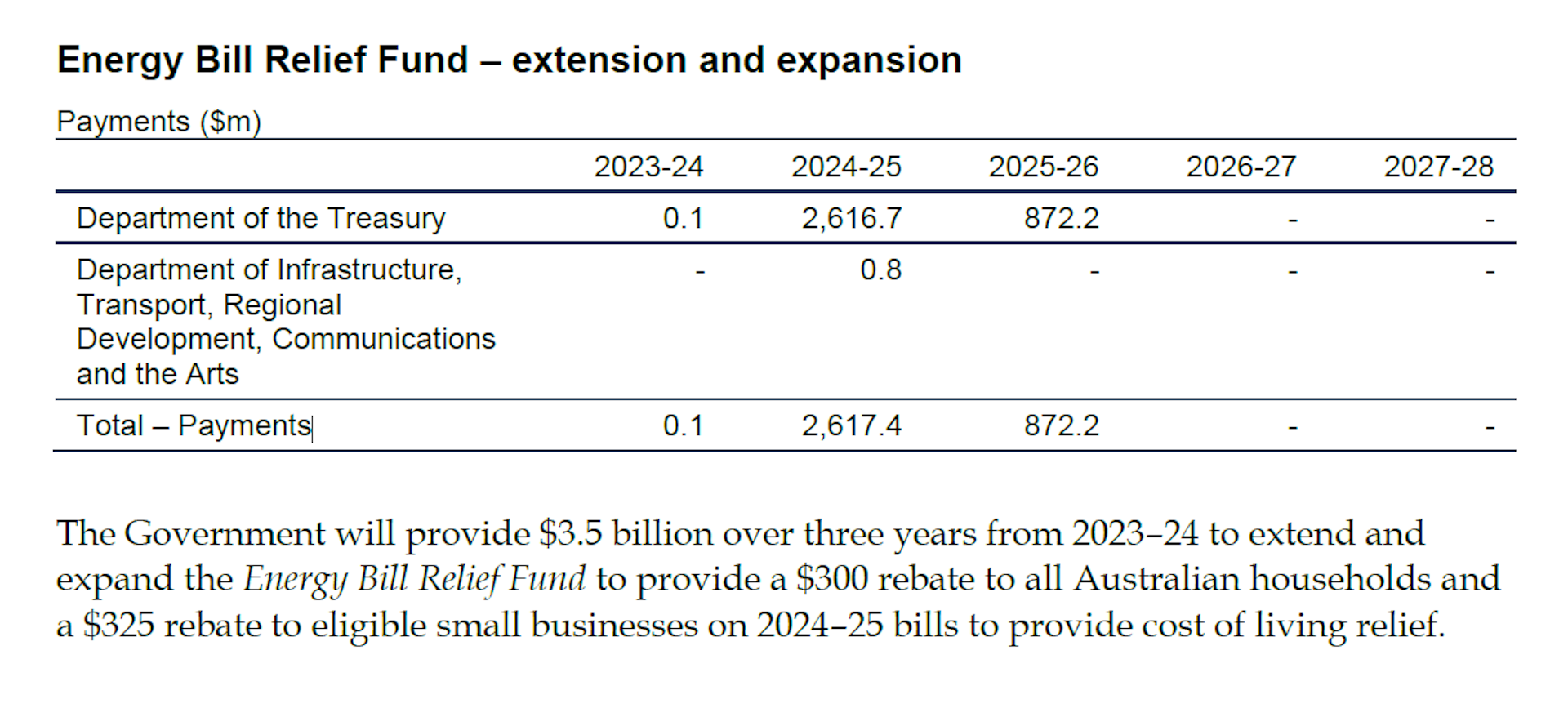

Treasury believes its measures to bring down the prices of rents[3], medicines[4] and energy[5] will cut the consumer price index by 0.5% percentage points.

But here, the plan hits an obvious snag. Providing relief on these expenses gives people access to the funds they would have spent on them. This, in turn, allows people to spend the money elsewhere, potentially adding to inflation.

So why does the treasury expect inflation to fall?

Some might save the budget handouts

Some people may not spend all of the money they save on rent, energy and medicines.

Reserve Bank researchers have found the government payments most likely to be spent are those that permanently boost incomes[6], especially those of lower-income households. The boost to rent assistance is one of those payments.

Temporary bonuses, such as the energy bill price relief, are less likely to be all spent and more likely to be saved.

Again, lower-income households[7] and households with less cash in the bank[8] are likely to spend more of what they are given than better-off households.

In addition, as the budget measures mechanically push down the consumer price index, they will also limit increases in government benefits that are linked to the index. This restrains future spending – and its effect on inflation.

Forecasts show the economy weak

But the main reason the treasury is confident its measures will restrain inflation lies deeper in the budget forecasts.

Two years of rising prices and interest rates have taken their toll on large numbers of Australians. As have two years of the government properly banking extra revenue in budget surpluses rather than providing more support to households.

Treasury has revised down its forecast of real household consumption growth this financial year from 1.5% in the last budget to just 0.25%, despite strong migration.

This means that, on average, each Australian is expected to buy less than they did a year ago, and substantially less than was previously expected.

Commonwealth Bank customer data shows working-age Australians have cut back dramatically[10] on spending in the first three months of this year, with only Australians aged 65 or more spending more in real terms. Many of these older Australians have been cushioned by owning their homes and having wealth that earns more when interest rates climb.

This is a pretty grim picture. One redeeming feature (until now) has been that unemployment has stayed low and employment has continued to grow[11], as it did in April, according to the figures released on Thursday.

But the labour market is showing signs of cooling. Average hours worked have fallen 3.5%[12] over the past year. Fewer employers are planning to hire[13], fewer are saying they find it hard to get new workers, and fewer are advertising.

Treasury expects unemployment to climb, moving from 4.1% to 4.5%[14] by the middle of next year. Although the unemployment rate would still be low by historical standards, the move up to 4.5% is a critical part of the inflation puzzle.

The budget also paints a pretty weak picture for the global economy, forecasting the longest stretch of below-average economic growth[15] since the early 1990s. This will bear down on the Australian economy, alongside any disruptions to trade as a result of geopolitical tensions around the world.

The lagged impact of the budget tightening over the past two years, growing unemployment and the subdued global outlook are all part of why the treasury is expecting inflation to come down and stay down.

More than mechanical

So, it isn’t just the mechanical effect of the budget measures on recorded prices. According to the treasury, the economy is set to cool as these measures are put in place, making knock-on spending pressures less likely than they would be in better times.

Forecasting is far from a precise science. Forecasting inflation is especially weird, given the role expectations about inflation play in bringing about actual inflation.

And forecasting turning points in the economy – such as when an economy that is overheating turns into one that is heading toward a recession – is especially difficult.

In this week’s budget, Treasurer Jim Chalmers has made a call that things are set to turn and he needs to change gears.

It’s a brave call, perhaps a fateful one with an election in the coming year. Only time will tell if its the economically wise one.

References

- ^ 2-3% target range (images.theconversation.com)

- ^ dropped dramatically (images.theconversation.com)

- ^ rents (images.theconversation.com)

- ^ medicines (images.theconversation.com)

- ^ energy (images.theconversation.com)

- ^ permanently boost incomes (www.rba.gov.au)

- ^ lower-income households (onlinelibrary.wiley.com)

- ^ cash in the bank (pubs.aeaweb.org)

- ^ Prostockstudio/Shutterstock (www.shutterstock.com)

- ^ dramatically (www.afr.com)

- ^ employment has continued to grow (www.abs.gov.au)

- ^ 3.5% (www.abs.gov.au)

- ^ planning to hire (www.rba.gov.au)

- ^ 4.1% to 4.5% (images.theconversation.com)

- ^ longest stretch of below-average economic growth (images.theconversation.com)

Authors: Aruna Sathanapally, Chief Executive, Grattan Institute, Grattan Institute

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}